Financial advice has long been a domain reserved for the wealthy — gatekept by complex jargon, high minimum investment thresholds, and opaque fee structures. But a new wave of thinking is changing all of that. Financial advice disfinancified is a growing movement that strips away the unnecessary complexity from personal finance guidance, making expert-level advice accessible, understandable, and actionable for everyday people.

Whether you are a first-time investor, a small business owner, or simply someone trying to make smarter decisions with your money, understanding financial advice disfinancified could reshape how you engage with your finances — and the professionals who guide them.

This article covers everything you need to know: what it means, how it works, global market trends, key features, pros and cons, and how to choose the right approach for your situation.

What Is Financial Advice Disfinancified? Understanding the Meaning

At its core, financial advice disfinancified refers to the simplification and democratization of financial guidance. The term combines “financial advice” with the concept of “disfinancifying” — a process of removing unnecessary financial complexity, industry jargon, and institutional barriers that traditionally make money management inaccessible to the average person.

Think of it as translating financial expertise into plain language. Instead of overwhelming clients with technical terms like “alpha-generating strategies,” “liquidity-adjusted returns,” or “correlation coefficients,” a disfinancified approach uses clear, everyday language to explain what those concepts actually mean for someone’s financial wellbeing.

The goal of financial advice disfinancified is not to dumb down financial planning — it is to make expert insight genuinely useful to a broader audience. This includes simplifying fee disclosures, using technology to deliver personalized guidance at scale, and shifting from transactional relationships to educational, empowerment-focused ones.

Key Concepts Behind the Term

- Democratization: Making quality financial advice available regardless of income level or wealth

- Simplification: Removing jargon and complexity without sacrificing accuracy or depth

- Transparency: Clear disclosure of fees, conflicts of interest, and recommendations

- Accessibility: Leveraging digital tools and platforms to reach underserved audiences

- Education-first: Prioritizing financial literacy as a foundation for better decision-making

Global Market Trends: The Rise of Financial Advice Disfinancified

The demand for simplified, accessible financial advice is not just a trend — it is a structural shift driven by demographic change, technological advancement, and a growing distrust of traditional financial institutions.

According to a 2023 report by Deloitte, over 60% of millennials prefer digital-first financial services over traditional banking relationships. Meanwhile, a study from the Financial Planning Association found that more than 70% of Americans feel overwhelmed by financial complexity — a gap that financial advice disfinancified is purpose-built to address.

Technology as the Key Enabler

The rise of robo-advisors, AI-driven financial planning tools, and fintech platforms has been instrumental in advancing the disfinancified model. Platforms such as Betterment, Wealthfront, and newer AI-powered advisory tools have reduced the minimum investment threshold from hundreds of thousands of dollars to as little as $1 — fundamentally altering who can access professional-grade financial guidance.

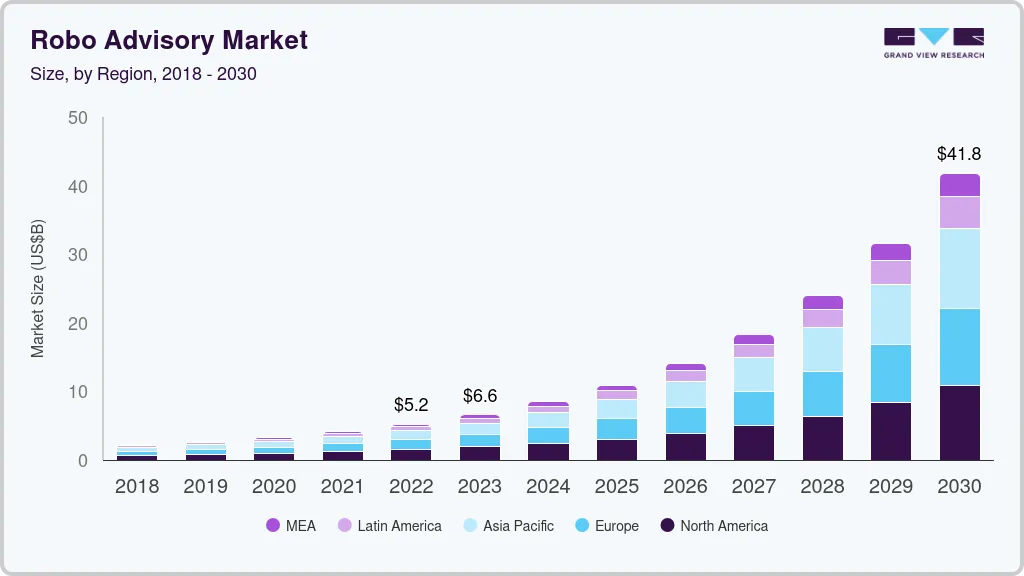

The global robo-advisory market was valued at approximately $7.4 billion in 2023 and is projected to surpass $72 billion by 2032, according to Allied Market Research. This explosive growth signals a market that is actively migrating toward simplified, technology-driven financial advice.

Regulatory Tailwinds

Global regulatory bodies are also pushing for greater transparency and simplicity. In the United Kingdom, the Financial Conduct Authority (FCA) introduced its Consumer Duty framework in 2023, requiring financial firms to deliver outcomes that are genuinely in the consumer’s best interest — a direct alignment with disfinancified principles. Similar initiatives are underway across the European Union, Canada, and Australia.

How Financial Advice Disfinancified Works

The mechanics of financial advice disfinancified differ meaningfully from traditional advisory models. Rather than relying solely on in-person consultations with credentialed advisors charging hourly fees, the disfinancified model integrates multiple delivery channels and methodologies to make guidance accessible.

Step 1: Plain-Language Assessment

The process typically begins with a straightforward financial health assessment. Instead of complex questionnaires filled with investment terminology, disfinancified platforms ask simple, relatable questions: How much do you earn each month? What are your biggest financial worries? What does financial freedom mean to you?

Step 2: Algorithm-Driven or Human-Augmented Recommendations

Based on the assessment, recommendations are generated — either by AI algorithms, human advisors, or a hybrid of both. The key differentiator is how those recommendations are communicated. Every suggestion is presented in plain English, with clear explanations of why the advice is being made and what impact it will have.

Step 3: Ongoing Education and Feedback Loops

Unlike one-time consultations, financial advice disfinancified emphasizes continuous engagement. Users receive educational content, regular progress check-ins, and simplified performance reports that focus on what matters — are you on track to meet your goals? — rather than overwhelming data dashboards.

Step 4: Transparent Fee Structures

Fees are presented upfront in dollar amounts, not percentage jargon. A platform might say, “You’ll pay $12 per month for this service” rather than “0.25% annual advisory fee.” This transparency is a foundational pillar of the disfinancified model.

Key Features of Financial Advice Disfinancified

Not all simplified financial advice platforms are created equal. The most effective implementations of financial advice disfinancified share the following core characteristics:

- Plain-Language Communication: All advice, reports, and recommendations are written in simple, jargon-free language that a non-expert can understand

- Low or No Minimums: Accessible to individuals regardless of their current wealth or income level

- Transparent Pricing: Flat fees or clearly explained percentage structures with no hidden costs

- Goal-Based Planning: Focus on personal financial goals rather than abstract market benchmarks

- Digital-First Delivery: Available via mobile apps, web platforms, or chatbots for maximum convenience

- Fiduciary Alignment: Recommendations made in the client’s best interest, not driven by product commissions

- Integrated Financial Literacy: Educational resources embedded directly in the advisory experience

- Human Escalation Options: Access to a real human advisor when complex situations arise

Pros and Cons of Financial Advice Disfinancified

Advantages

- Accessibility: Brings quality financial guidance to individuals who were previously excluded due to cost or complexity

- Clarity: Eliminates confusion and helps clients understand exactly what actions they should take and why

- Lower Costs: Digital delivery and automation reduce overhead, allowing platforms to serve clients at a fraction of traditional advisory costs

- Empowerment: Clients who understand their financial situation are better positioned to make informed decisions independently

- Scalability: Technology enables advisors and platforms to serve thousands of clients simultaneously without sacrificing personalization

- Trust Building: Transparency in fees and recommendations fosters stronger client-advisor relationships

Limitations to Consider

- Oversimplification Risk: In rare cases, stripping away complexity may omit nuances that are critical for high-net-worth individuals or those with complex tax situations

- Limited Depth for Edge Cases: Highly specialized financial scenarios — such as cross-border taxation or complex estate planning — may require more traditional, in-depth advisory support

- Algorithm Dependency: Fully automated models may not account for emotional or behavioral factors that a human advisor would naturally recognize

- Regulatory Variability: The disfinancified model is advancing at different speeds globally, meaning access and quality can vary significantly by region

How to Use and Choose the Right Financial Advice Disfinancified Approach

If you are considering adopting a disfinancified financial advice model — whether as a consumer or as a financial professional looking to modernize your practice — here is a practical framework to guide your decision.

For Individual Consumers

- Identify Your Primary Goal: Are you looking to get out of debt, build an emergency fund, invest for retirement, or all three? The best disfinancified platforms are goal-driven.

- Evaluate the Language: Before committing to any platform or advisor, review sample content. Can you understand it easily? If not, keep looking.

- Check Fee Transparency: Always ask for a complete fee disclosure in dollar terms before signing up. Beware of platforms that only quote percentage-based fees without context.

- Assess the Fiduciary Standard: Confirm that the advisor or platform is legally required to act in your best interest, not just recommend “suitable” products.

- Look for Education: The best disfinancified platforms do not just give you answers — they help you understand why those answers are right for your situation.

For Financial Professionals

- Audit Your Communications: Review your client-facing materials and identify jargon-heavy language that can be simplified without losing accuracy.

- Invest in Client Education Tools: Incorporate financial literacy resources — videos, glossaries, interactive tools — into your client experience.

- Consider Technology Partnerships: Explore integration with fintech platforms that can help automate routine advice delivery, freeing you to focus on complex, high-value client relationships.

- Adopt Transparent Fee Models: Move toward flat-fee or subscription-based pricing that clients can understand intuitively.

Comparison: Traditional vs. Disfinancified Financial Advice

Traditional financial advice typically involves: in-person meetings, complex reports, high minimum asset requirements, commission-based compensation, and technical language. Financial advice disfinancified, by contrast, emphasizes: digital accessibility, plain-language communication, low or no minimums, transparent flat-fee models, and continuous financial education.

Frequently Asked Questions (FAQs)

1. Is financial advice disfinancified suitable for high-net-worth individuals?

Yes, though with some nuance. While financial advice disfinancified is primarily designed to improve accessibility for everyday consumers, high-net-worth individuals also benefit from clearer communication, transparent fees, and education-driven engagement. That said, those with complex estate planning needs, multi-jurisdictional tax obligations, or sophisticated investment portfolios may still require traditional advisory support in addition to a disfinancified layer.

2. How does financial advice disfinancified differ from robo-advice?

Robo-advice is one delivery mechanism within the broader financial advice disfinancified framework, but the two are not synonymous. Disfinancified advice can be delivered by human advisors, hybrid models, or fully automated platforms. The defining characteristic is not the technology used — it is the commitment to simplicity, transparency, and accessibility in how that advice is communicated and delivered.

3. Can financial advisors adopt a disfinancified approach without losing revenue?

Absolutely. Many financial professionals find that simplifying their communication and moving toward transparent pricing actually increases client retention and referral rates. Clients who understand and trust their advisor are far more likely to consolidate their financial relationship — bringing more assets under management and recommending the advisor to friends and family. Disfinancification is not a threat to advisory revenue; it is a growth strategy.

4. Is financial advice disfinancified regulated?

The underlying financial advice is regulated in the same way as any other advisory service — advisors must still hold appropriate licenses and comply with fiduciary or suitability standards depending on their jurisdiction. What disfinancification changes is the communication style and delivery model, not the regulatory framework. If anything, global regulators are increasingly encouraging simpler, more transparent advice — making disfinancified practices more aligned with the regulatory direction of travel.

5. How do I know if a platform offering financial advice disfinancified is trustworthy?

Look for the following indicators of credibility: regulatory registration with the relevant financial authority in your country, a clearly stated fiduciary commitment, verifiable fee disclosure, positive client reviews and independent ratings, and evidence of ongoing education resources. Avoid platforms that make unrealistic return promises, obscure their fee structures, or pressure you into immediate decisions. A genuine disfinancified approach puts your understanding and confidence first.

Conclusion: The Future of Finance Is Clear, Not Complex

Financial advice disfinancified is not a passing trend — it is a fundamental redefinition of what good financial guidance looks like in the modern era. By removing unnecessary complexity, prioritizing transparency, and empowering individuals with knowledge rather than overwhelming them with jargon, the disfinancified model is making it possible for more people than ever before to achieve genuine financial confidence.

Whether you are an individual looking for trustworthy, understandable financial guidance, or a financial professional ready to modernize your practice, the principles of financial advice disfinancified offer a clear, proven path forward.

Ready to experience financial advice that actually makes sense? Start by auditing your current financial relationships — and ask yourself: do I understand exactly what advice I am getting, why I am getting it, and what it is costing me? If the answer is no, it is time to explore a more disfinancified approach.